The African Remittance Dilemma: Innovation at a Cost

March 28, 2025

At first glance, Africa’s remittance economy appears to be thriving. Diaspora inflows into Sub-Saharan Africa reached an estimated $54 billion in 2023, representing lifelines for households, school fees, micro-entrepreneurship, and rural healthcare. But beneath the numbers lies a murky landscape: persistent remittance costs averaging over 6.35% [1], bureaucratic FX restrictions, and an aging correspondent banking system struggling to remain relevant in a digital-first era. For millions, the promise of financial inclusion remains hostage to antiquated rails.

Every year, African families receive over $100 billion in remittances from loved ones abroad. These flows often account for up to 10% of GDP in countries like The Gambia, Lesotho, and Somalia, making them more than just cash—they are the oxygen lines of economic survival. Yet, ironically, sending money to Africa remains one of the most expensive financial activities in the world.

Based on World Bank data, the average cost of remitting $200 to Sub-Saharan Africa was 6.35% in 2023, nearly double the global target set by the UN’s Sustainable Development Goals (SDG 10.c). This inefficiency persists despite a digital revolution. While mobile money platforms have narrowed the gap in certain corridors, commercial banks and traditional MTOs still dominate the landscape—and they charge handsomely for the privilege.

This, perhaps more than any other reason, is why stablecoins have entered the African financial imagination not as novelty, but as necessity. Backed by fiat, borderless by nature, and increasingly integrated into mobile-first economies, stablecoins are quietly rewriting the rules of remittances—starting not from the top-down, but from the informal trenches of peer-to-peer trade, hustler economies, and migrant money flows.

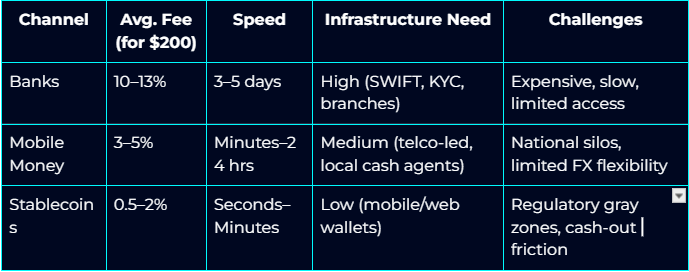

Banks: The Costly Gatekeepers of Cross-Border Flows

For decades, commercial banks were the default option for international money transfers. But data from the World Bank’s Remittance Prices Worldwide Database [2] paints a troubling picture:

- In Q4 2023, banks charged an average fee of 10.74% to send money to Sub-Saharan Africa.

- Add currency conversion markups and settlement delays, and that number often climbs past 13%.

- These fees disproportionately impact low-income migrants, many of whom send under $300 per transaction.

Moreover, correspondent banking relationships—a backbone of cross-border settlements—have been in steady retreat. Between 2011 and 2019, Africa experienced a 27% drop in correspondent banking corridors, according to the World Bank [3]. Fewer corridors mean reduced competition, higher spreads, and delayed settlements.

Consequently, banks have lost ground—not due to lack of infrastructure, but due to poor alignment with the economic realities of African households.

Mobile Money: The Middle Path to Affordability

Mobile money has long been hailed as Africa’s fintech marvel. Services like M-Pesa, MTN MoMo, and Orange Money have democratized access to domestic financial services, even in rural and low-income communities. For cross-border transfers, they’ve made a measurable dent in cost.

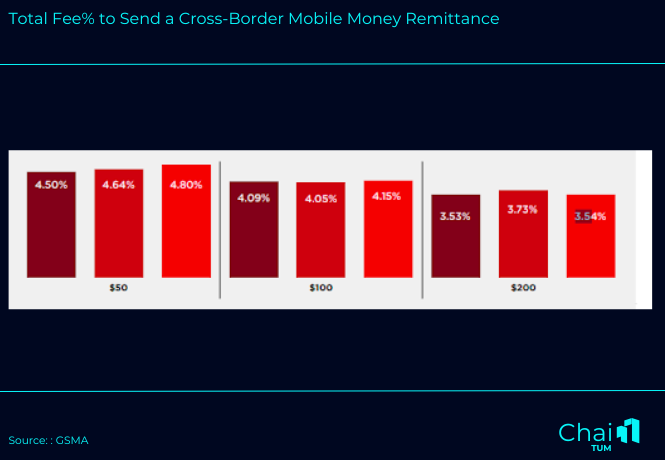

According to the GSMA Cross-Border Mobile Money Report [4]:

- Average fees for sending $200 through mobile money fell to 3.54% in 2023 as shown in Graph 1.

- This is significantly lower than banks or MTOs and well within reach of the SDG target.

- In certain corridors (e.g., Uganda–Kenya), transfer costs dropped below 2.8%.

Graph 1

Still, mobile money has its limitations:

- Many services lack interoperability across borders or currencies.

- Liquidity constraints and cash-out fees reduce cost transparency.

- Most platforms still rely on national mobile networks, restricting their continental scale.

Thus, while mobile money has expanded financial inclusion domestically, its potential as a true cross-border disruptor remains capped by structural fragmentation.

Stablecoins - Remittance Workhorse

Stablecoins—cryptocurrencies pegged to fiat currencies like the USD or EUR—are redefining what’s possible in remittance rails. By removing traditional intermediaries, they enable peer-to-peer value transfer in real time, with no reliance on correspondent banks or FX dealers.

Based on Chainalysis [5] and Obiex/Quidax [6][7] analyses:

- Stablecoins are already used in over 9% of crypto-based remittances into Africa.

- Transfer costs using stablecoins often range from 0.5% to 2%, depending on the platform and method of cash-out.

- They settle in seconds, not days, and can be accessed using low-cost mobile wallets or even browser-based apps.

In informal corridors like Nigeria–Ghana or Kenya–Uganda, Telegram P2P bots, WhatsApp crypto groups, and crypto-friendly fintech platforms now facilitate stablecoin transfers that settle faster and cheaper than most licensed money transfer operators (MTOs).

For example, Obiex allows Nigerians to receive stablecoin-based remittances and cash out in naira instantly—without ever touching a bank. Similarly, Paxful and Yellow Card enable stablecoin transfers between Ghana, Nigeria, and South Africa using local agent networks.

Nonetheless, the total volume of stablecoin transactions in Africa grew by over 60% in 2023 alone —a strong signal that utility is winning over hype.

Comparative Analysis: Cost, Speed, and Reach

Stablecoins outperform across all key metrics—except regulation. They win on cost, speed, scalability, and global compatibility. However, without clear rules of engagement, their broader impact will be muted or confined to informal channels.

Stablecoins and the $100B Opportunity

If stablecoins were to capture just 25% of Africa’s $100B remittance market, that would translate into $25 billion in annual flows—potentially saving over $2 billion in transaction fees every year.

Moreover, as pilot projects like the USDC Africa Remittance pilot show, stablecoins aren’t just cheaper—they’re programmable. Funds can be tagged for school fees, medical payments, or savings accounts, enabling conditional transfers and transparency that banks simply cannot match.

Ultimately, this is not just about replacing remittance providers. It’s about redefining financial sovereignty—giving families, freelancers, and traders across Africa control over how, when, and in what currency they get paid.

Yet… the Risk Ledger Is Not Empty

Despite the upside, stablecoins are no panacea. Stablecoin operations remain heavily dollarized, exposing African economies to external monetary policy shocks. Moreover, stablecoins are often issued by offshore entities, meaning local regulators have minimal oversight or recourse in case of fraud, asset freezes, or mismanagement of reserves.

Then there’s the trust gap. Most Africans have never seen a “Circle” or “Tether” office. User adoption is often based on community testimonials, not institutional trust. Without robust education and public-private frameworks, stablecoins risk being seen as speculative tools rather than daily instruments of value exchange.

Furthermore, cash-out fees—though lower in mobile money corridors—remain volatile. According to GSMA, regions like West and Central Africa have seen recent increases in agent-based cash-out fees, especially for $50 transactions. This suggests a creeping trend where operators recoup revenue losses through ancillary fees—undermining the cost-efficiency narrative unless addressed.

Thus, the path forward hinges on three strategic pivots:

- Stablecoins must be embedded within mobile apps people already use—Chipper Cash, M-Pesa, MoMo, and even traditional bank apps. This reduces friction, boosts credibility, and accelerates adoption.

- Instead of blanket bans, governments should follow sandbox models like those in South Africa, testing stablecoin use cases in controlled corridors and crafting region-specific guidelines [10]. African regulators must ask: can we tax, monitor, and license stablecoins, rather than criminalize them?

- Platforms like PAPSS (Pan-African Payment and Settlement System) offer an opportunity. If paired with stablecoin rails, they could power compliant, continent-wide settlements for SMEs, schools, health systems, and diaspora remittances—without needing Western intermediaries.

Conclusion: The Next Remittance Rail Is Already Online

Stablecoins, in their current trajectory, are neither replacements for fiat nor disrupters of central banks. They are pragmatic financial tools, designed to solve deeply African problems with elegantly digital solutions.

Chaintum concludes that most successful digital money ecosystems won’t be those with the flashiest tech, but those that solve real friction for real people. In this regard, stablecoins may prove more transformative than any development aid, more impactful than any single fintech unicorn.

Stablecoins are no longer a side show—they are the new benchmark, and unless traditional players evolve fast, they’ll become irrelevant in the corridors that matter most.

As regulators deliberate and fintechs experiment, the question isn’t whether stablecoins will reshape African remittances. It’s whether everyone else can catch up.

Want to stay ahead of the curve and learn more about this groundbreaking innovation? Subscribe to our newsletter and follow us on X and LinkedIn to join the conversation and be part of the future of real estate in Africa.

Subsribe To Our Newsletter

Get the Inaugural Edition of Chaintum Magazine Right at Your Inbox